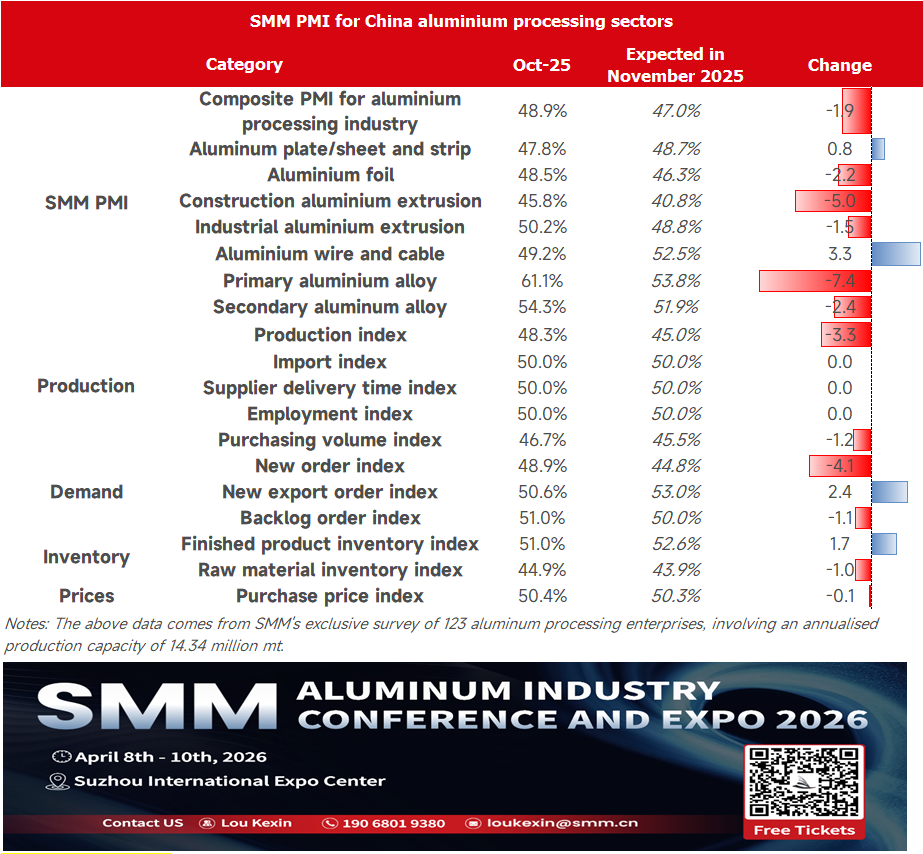

In October, the aluminum processing composite PMI fell 6.8 percentage points MoM to 48.9%, dropping below the 50 mark. PMIs for most aluminum processing sectors declined significantly into contraction territory, mainly due to weakening end-use demand and high aluminum prices suppressing activity. By sector, aluminum plate/sheet and strip faced simultaneous pressure on both production and demand, with declining construction sector orders and high aluminum prices fueling wait-and-see sentiment, leading to notable inventory pressure. Aluminum foil saw insufficient supply and demand momentum; double zero foil order declines dragged down the overall performance, with only export stockpiling providing some buffer, while expectations for processing fee increases emerged. Construction extrusions continued to be weighed down by industry sluggishness; the National Day holiday reduced production days, and falling temperatures in northern regions will further impact subsequent project progress. Industrial extrusion barely remained above the 50 mark, with limited support from automotive orders and a sharp drop in PV extrusion production. Aluminum wire and cable experienced poor end-user cargo pick-up and high aluminum prices suppressing the operating rate; although expectations for accelerated State Grid tenders exist, short-term demand release remains uncertain. Primary alloy and secondary alloy maintained expansion, mainly relying on domestic demand recovery and inventory optimization. Driven by the September peak season, primary alloy saw active production scheduling, sustained domestic demand recovery, and significant inventory drawdowns, though enterprises remained cautious about capacity expansion. Secondary alloy benefited from resilient downstream automotive demand, with large plants maintaining high operating rates; although small and medium-sized enterprises were constrained by raw materials and costs, low inventory provided support for the future.

By product type:

Aluminum plate/sheet and strip: In October, the aluminum plate/sheet and strip PMI was 47.8%, down 11 percentage points MoM, falling sharply into contraction territory. Among the sub-indices, both the production index and the new orders index stood at 45.9%, indicating simultaneous pressure on production and demand. The new export orders index was slightly above the 50 mark at 51.4%, reflecting relative stability in the export market, though insufficient to reverse the overall weakness. In terms of monthly operations, early in the month, supported by the traditional September-October peak season, leading enterprises demonstrated strong production resilience, with new energy-related production lines such as automotive sheet and battery shells operating at near full capacity. However, by mid-to-late October, construction-related segments like curtain wall panels were dragged down by funding chain pressures and a rapid decline in orders, becoming the main factor lowering the operating rate. Meanwhile, aluminum prices rising to the 21,000–21,200 yuan/mt range intensified downstream wait-and-see sentiment, with the purchasing volume index at only 45.9%, indicating more cautious raw material purchasing by enterprises. The product inventory index remained high at 57.8%, highlighting significant destocking pressure. Overall, as the industry approaches the transition period between peak and off-seasons, expectations of weakening demand are strengthening, and the aluminum plate/sheet and strip PMI is expected to remain below the 50 mark in November.

Aluminum foil: In October, the aluminum foil PMI was 48.5%, down 14 percentage points MoM, falling sharply into contraction territory. Both the production index and the new orders index stood at 47.5%, pointing to weak momentum on both the supply and demand sides. The new export orders index was 51.1%, benefiting from overseas holiday stockpiling demand for Halloween and Thanksgiving, which provided some cushion for packaging foil and container foil exports. Within the month, enterprise operations showed significant divergence: industrial demand-oriented production lines such as battery foil and brazing foil maintained stable orders, supporting steady operating rates among leading enterprises. However, double zero foil orders declined due to an early end to the peak season, dragging down overall performance. The raw material inventory index was 46.4%, and the purchasing volume index was 46.4%, reflecting cautious stockpiling strategies among enterprises. Notably, the issue of processing fees has emerged; affected by declining yield rates, battery foil processing fees are expected to increase in the new year. As the effect of overseas holiday stockpiling gradually diminishes, the operating rate in the aluminum foil industry is expected to decline slightly, and the aluminum foil PMI is projected to remain below the 50 mark in November. Construction aluminum extrusion: The composite PMI for construction aluminum extrusion in October registered 45.79%, remaining below the 50 mark. According to an SMM survey, although some small enterprises in Hebei and Hunan reported an increase in aluminum formwork orders, the overall industry remained sluggish. Coupled with the fact that construction aluminum extrusion enterprises generally had fewer production days due to the extended National Day holiday, the production index for the month recorded 41.99%, and the new orders index was 43.83%. Regionally, some medium and large building material enterprises in Guangdong and Shandong operated relatively steadily, while some small enterprises in North China reported a decline in building material orders in October. As the seasonal transition occurs, compounded by the impact of falling temperatures in the north on construction progress, related enterprises have weak expectations for November production. The construction aluminum extrusion PMI is expected to remain below the 50 mark in November.

Industrial extrusion: The composite PMI for the industrial extrusion industry in October was 50.23%, barely staying above the 50 mark. The production index for the month recorded 48.83%. In late October, some enterprises in East China and South China reported that year-end pushes by downstream automakers led to a slight increase in orders for automotive parts, providing some support to the operating rates of related enterprises. For PV extrusion, major aluminum frame extrusion enterprises in Anhui and Hebei saw production drop by 20–30% this month due to production cuts by downstream module manufacturers. Some solar panel mounting bracket enterprises in Fujian reported that their products are mainly exported to Southeast Asia and Europe, and performance is currently relatively stable. Looking ahead to November, demand for PV extrusion remains weak, while the rail transit and 3C industries are operating steadily, and the automotive, ESS, and power sectors are relatively robust. However, due to the recent high aluminum prices, existing orders for enterprises are mostly maintained at around one week, and expectations for November are generally weak. The industrial extrusion PMI is expected to fall below the 50 mark.

Aluminum wire and cable: The PMI for China's aluminum wire and cable industry in October recorded 49.2%, falling below the 50 mark, indicating a pullback in industry sentiment. Poor end-user cargo pick-up and high aluminum prices suppressing operating rates were the main drags. In production, affected by losses and slower shipments, the production index fell sharply by 22.1% MoM to 53.8%. Although the new orders index increased by 5.4% MoM to 53.69%, the order fulfillment pace was hindered by poor end-user pick-up. The finished product inventory index was 47.67%, indicating insufficient willingness among enterprises to build inventory, and the purchasing volume index dropped to 45.34% as operations contracted. High aluminum prices pushed up costs, with the purchase price index at 50.6% squeezing profits and further inhibiting production. As November begins, orders from State Grid will enter the tender opening phase. By year-end, the task of completing 650 billion yuan in power grid investment needs to be fulfilled, and the tender pace is expected to accelerate, which is favorable for enterprises to secure more orders. However, currently, as year-end approaches, project demand performance remains generally tepid, and the release of end-use demand still needs to be awaited. If end-user pick-up and the aluminum price trend do not improve, the industry may remain under pressure. Subsequent attention should be paid to marginal changes in aluminum prices and end-use demand. Primary alloy: In October, the primary aluminum alloy PMI reached 61.1%, up 1.4 percentage points MoM from September, indicating a continued recovery in the industry. Sub-index analysis shows the production index surged to 74.1%, while the new orders index rose to 68.8%, reflecting active production scheduling by enterprises and sustained recovery in domestic demand against the backdrop of the September peak season. New export orders remained at the 50 mark, indicating stable external demand. Notably, the finished product inventory index pulled back to 39.6%. Combined with the purchasing volume index of 58.3%, this suggests effective inventory reduction by enterprises and a more positive stockpiling sentiment. Although auxiliary indicators such as the import index and purchase prices remained at the 50% threshold, the overall structure demonstrated active production and smooth inventory reduction. However, the raw material inventory index held steady at 50.0%, indicating that enterprises remain cautious about expanding production. Against a backdrop of weakened support from previous liquid aluminum conversion and persistent pressure from high aluminum prices, the industry has entered the traditional peak season, but cost-side pressures remain, and the foundation for overall improvement is not yet solid. Looking ahead, as the industry enters the off-season in November, the PMI is expected to pull back slightly but remain above the 50 mark.

Secondary alloy: In October, the secondary aluminum industry PMI fell 6.9 percentage points MoM to 54.3%, but remained above the 50 mark. Demand side, orders from downstream sectors such as automotive remained stable with a positive trend. Although the increase was limited, overall demand showed strong resilience. Supply side, the operating rate varied significantly among enterprises. Some, especially large manufacturers, maintained high operating rates, but small and medium-sized enterprises faced multiple constraints: ① Holiday effect: The National Day holiday shortened effective production time; ② Raw material bottleneck: Tight market supply kept enterprise inventories persistently low, making restocking difficult and limiting capacity release; ③ Cost pressure: High raw material prices squeezed profits, and weak finished product price increases forced enterprises to proactively cut production; ④ Policy disruptions: Some enterprises in Henan, Jiangxi, and other regions continued production cuts or suspensions due to policy uncertainty; ⑤ Environmental constraints: Environmental protection warnings in Hebei and other regions triggered localized production restrictions by month-end. Inventory side, both raw material and finished product inventories remained at low levels. Looking ahead to November, expectations of a push for annual targets by end-users at year-end are expected to boost secondary aluminum demand. Coupled with support from low inventory levels, the industry PMI is likely to maintain its expansion trend.

The PMI for the aluminum processing industry in October was recorded at 48.9%, as the October peak season fell short of expectations and re-entered contraction territory. This was mainly due to factors such as aluminum prices fluctuating at highs, weak construction demand, and weakening export momentum. Looking ahead to November, the industry is expected to continue its divergent pattern, with the composite PMI likely to decline further to 47.0%. From the perspective of core influencing factors:

- On the demand side, the transition from the peak to off-season, coupled with falling temperatures in northern regions, has led to persistently weak demand in construction and some industrial sectors.

- On the cost side, aluminum prices fluctuating at highs have suppressed downstream purchase willingness, squeezing enterprise profit margins.

- On the structural side, demand in areas such as new energy and automobiles remains relatively stable, providing important support for certain products.

Moving forward, close attention should be paid to the impact of aluminum price trends on downstream cargo pick-up sentiment and the marginal improvement in end-use demand.